Embodied Carbon: A Strategic Priority for the Real Estate Sector

Managing embodied carbon: an essential lever for the environmental transition of real estate

As regulatory pressure around embodied carbon intensifies, one thing is clear: the transition toward precise management of this indicator could be faster, despite its strategic relevance for all players in the real estate value chain. Between legal obligations and business transformation, where do we really stand?

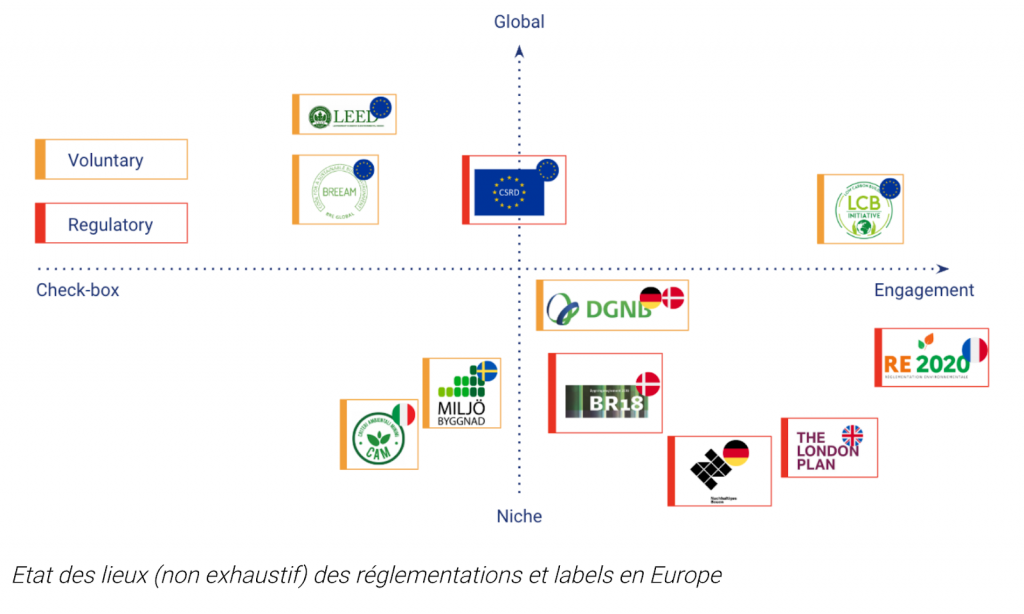

I. Intensification of regulations and labels on embodied carbon

All regulations and labels, at both corporate and project levels, are moving toward more granular embodied carbon calculations:

- The Taxonomy, which makes carbon a criterion for analyzing “green” activity and encourages or discourages companies regarding loan allocation.

- The CSRD, which stems from the Taxonomy and requires companies to report their emissions and justify a decarbonization plan across all emission scopes.

- The RE2020, which imposes methodology and thresholds at the scale of new construction operations.

- Labels such as BBCA (new and renovation) or LCBi, which require a specific methodology and thresholds to be met, with a score based on results.

- The CRREM, which makes embodied carbon a new evaluation criterion and proposes the SBTi as a reference framework.

Going beyond regulatory requirements, more and more decision-makers (funds and asset managers) are conditioning their investments on carbon performance, moving past standard requirements for environmental performance. Embodied carbon is becoming a strategic indicator to master.

II. Structural inertia fueled by the complexity of the subject

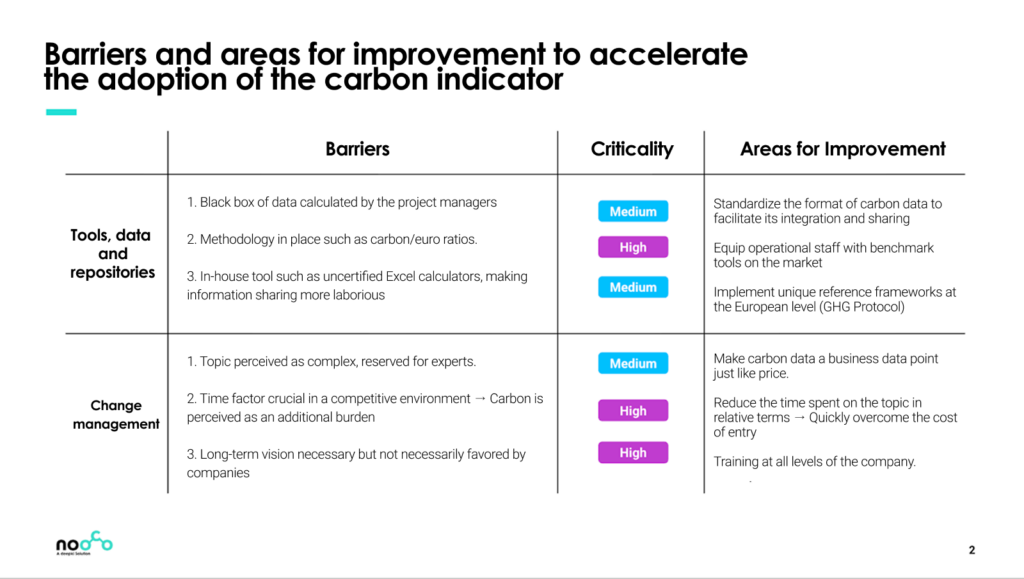

Despite increasingly strong regulatory obligations and a market aware of the structural changes needed to reach environmental goals, many obstacles persist. Below is a non-exhaustive list of barriers and areas for improvement regarding the more widespread adoption of the embodied carbon indicator.

In summary, there are 3 major obstacles to the generalization of carbon calculation across all players in the value chain:

- A calculation that is still poorly understood or poorly communicated by the stakeholders in charge.

- Tools/methodologies specific to each user, which hinder the consolidation of a common framework and the sharing of carbon information.

- An additional burden (cost and time) generated by carbon calculation, perceived as time-consuming with current methods.

We have considered 3 avenues to address these challenges, listed here without detailing the specific modalities:

- Standardization of data formats to facilitate integration within different tools and sharing.

- The implementation of a common reference framework at the European scale, for all types of construction operations at the project and corporate levels.

- Reducing the entry cost for setting up calculation processes by improving existing tools and streamlining the practices of stakeholders.

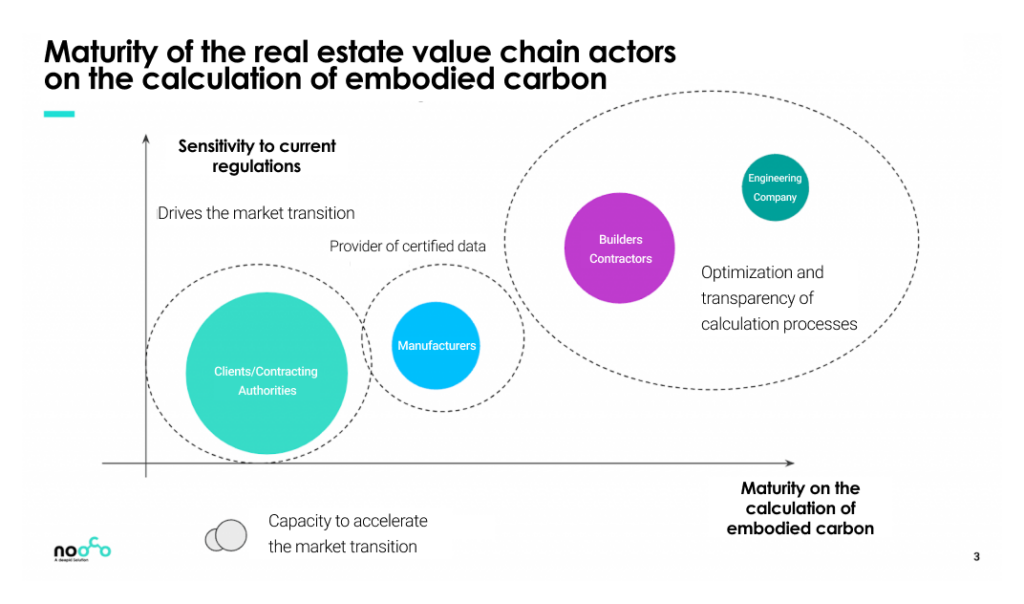

III. Construction stakeholders: varying levels of maturity according to regulatory sensitivity

Below is a non-exhaustive mapping of the actors in the real estate value chain. The objective of this visual is to present their role in the embodied carbon calculation process and their maturity based on their sensitivity to current regulations.

All players in the value chain are essential to the market transition:

- Decision-makers, the market drivers, by proposing a long-term strategic vision for investments and integrating contractual carbon requirements.

- Manufacturers, providers of carbon data on materials and equipment, indispensable for continuously improving calculations and making them simpler to perform.

- Contractors and engineering firms, often in charge of the embodied carbon calculation, must continue to demonstrate that optimized and transparent calculation processes are possible and must become the norm.

While maturity levels vary and are not yet sufficient, this is notably because short-term market logics hinder the full appreciation of non-compliance risks as well as those related to climate change.

However, managing these risks is key, especially for decision-makers, because reducing vulnerabilities is a lever to ensure asset value.

Conclusion

Ultimately, while there is inertia within the real estate market regarding embodied carbon calculation, many positive signals show that players are mobilizing to address the subject. Structural and cyclical difficulties are well-identified, as are the paths to instating better control of the carbon indicator into standard practices.

It remains necessary to continue engaging all stakeholders in the value chain to accelerate the market transition. This involves solutions like Nooco, which makes carbon calculation scalable within complex organizations and optimizes time spent and information sharing. We work daily to create the shift that will finally make carbon calculation a standard practice, on par with more traditional financial indicators.